Insider alert! I am making a move on a 💲Value Stock.

2 weeks ago I made a whole post on why I like so much tracking insiders´ transactions, and why I mainly look at buyers rather than sellers. Since April there were not many insiders buying signals, so I had to broaden my investing skills to find new opportunities. This is one of the things I love about investing, it is so dynamic that you always are invited to question your knowledge and incentivize to learn every day.

Cheap VS Expensive (Value VS Growth) stocks investing strategies.

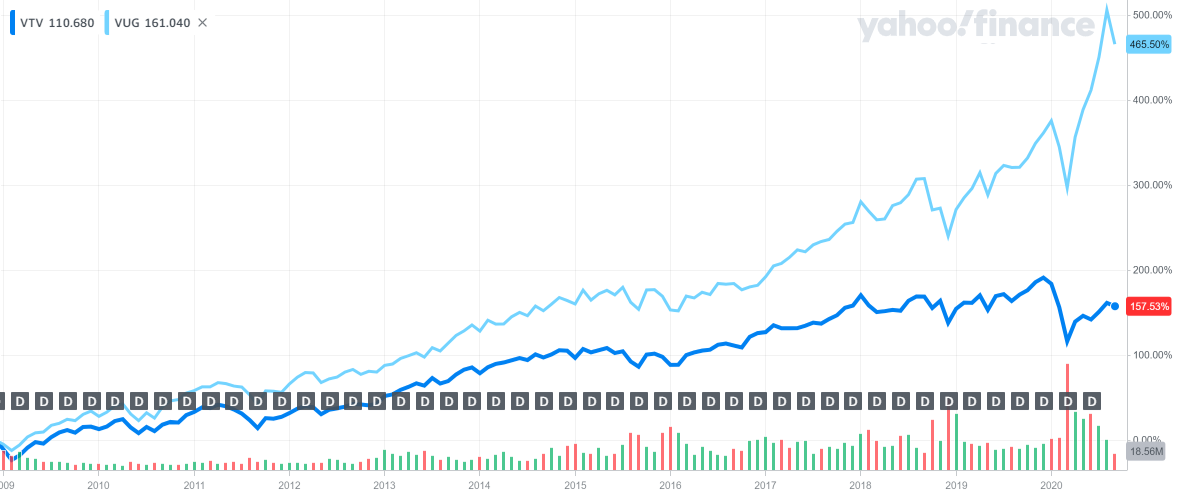

About a month ago, I was looking beyond my usual suspects and got a look at "value stocks". What Is a Value Stock? A value stock is a stock that trades at a lower price (aka cheap) relative to its fundamentals, such as dividends, earnings, or sales. Pretty much what we should be looking for all year long when investing right? Well not necessarily if you compare its track record with its alternative: "growth stocks". Growth stocks are stocks known for over pacing the industry average revenue growth, but for which you have to pay a premium (aka expensive) compared to its peers. If we simplify both kinds of stocks to the Vanguard ETF equivalent, "VTV" for value stocks and "VUG" for growth stocks, you will get something like this: since 2004 growth stocks beat value stocks 3 to 1 in terms of total return without dividend reinvestment. According to LazyPortfolio, if we consider dividends yields, 1000 USD invested in VTV (value stocks) back in 2004 would have grown to 3436 USD in August 2020, while the same investment in VUG (growth stocks) would have grown to more than 6000 USD.

Growth also means volatility

Based on the previous data, my portfolio is mainly composed of growth stocks but, it also comes at a price: volatility. This is why market corrections hurt so much when you are growth-focused. With so much uncertainty ahead, I got motivated to look at some opportunities in value stocks to diversify (a little) away from Tech and lower my portfolio volatility. Note that this is not a change of strategy, I will remain growth-focused as it better fits my investing plans.

This will be a secondary strategy I may add it to along the way if it works.

Building a Value Stocks watchlist

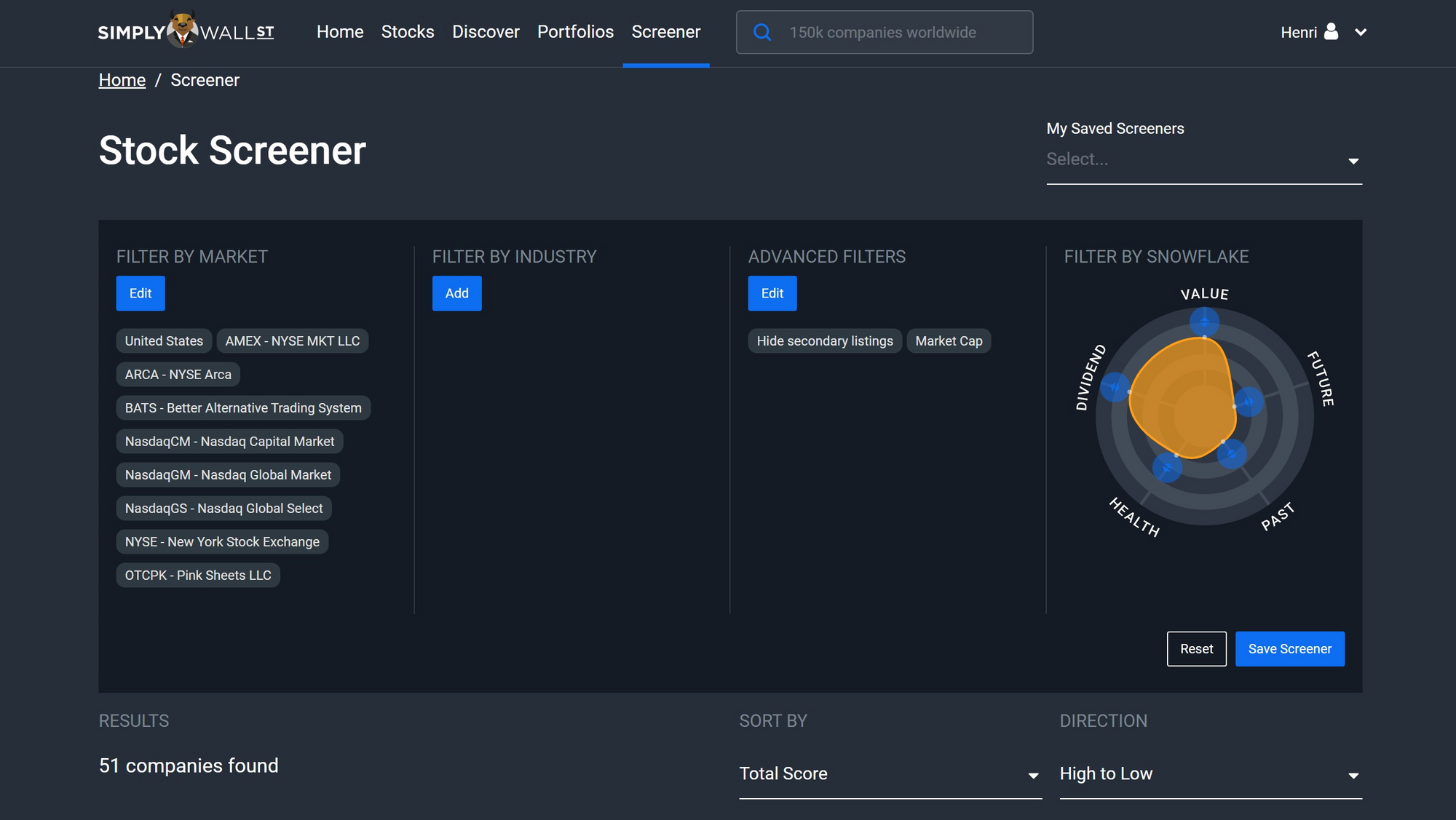

The first thing I made was building my watchlist of value stocks. How? I use SimplyWall.st screener like this:

You do have to be careful though, as great value usually comes with a great caveat. For example, one of the greatest values now, according to SimplyWall.St, is INTEL. This is in part because many are critics about its outlook after big troubling news about manufacturing delays with the 7-nanometer chips. "Is INTEL a buy?" is not the matter of this post, but here is another columnist take on it.

I built my own watchlist combining the value screener with some market trends that I expect to materialize in the near term.

One MEGA trend that made me add storage facilities REITs to my watchlist

Distribution centers are being built at an infernal rate by the likes of Amazon, Walmart, DHL and many more. Competing with the one-day delivery democratized by Amazon takes storage a key part of the e-commerce growth. There are 2 main and complementary strategies to manage that kind of fast delivery experience: almighty distribution centers and last miles storages (aka storage closer to the final customer in urban areas). Ron She, managing director and associate portfolio manager at Duff & Phelps Investment Management Co puts it this way:

Warehouse space is limited, especially near dense urban areas, and financing new industrial real estate is not as easy as it was before the financial crisis. Add this to the booming e-commerce industry, and you're left with a recipe for the rising rents and record-low vacancy rates that lead to burgeoning profits.

Besides the surge of e-commerce, the warehouse real estate industry has another tailwind: the need for greater resiliency. Shocks like COVID, tsunamis, earthquakes, storms etc. put great stress on global supply chains, and convinced businesses to keep more inventory on hand to avoid running out of key parts. Chris Caton, senior vice president of global strategy and analytics at Prologis (The biggest REIT with industrial warehousing real estate) says “that is going to be a defining characteristic of the industry over the coming years. More inventory, of course, means more demand for a place to put it."

Last but not least, the Goldman Sachs investment fund just bought 3 Million square feet of urban land to be transformed into facilities to support last-mile deliveries of online orders.

This is the reason why I felt pretty excited when I saw that Public Storage Facilities (PSA), one the leader in self-storage (by definition urban warehouses), is a value stock.

How PSA made it to the top of my watchlist, then fall. Meet their competitor

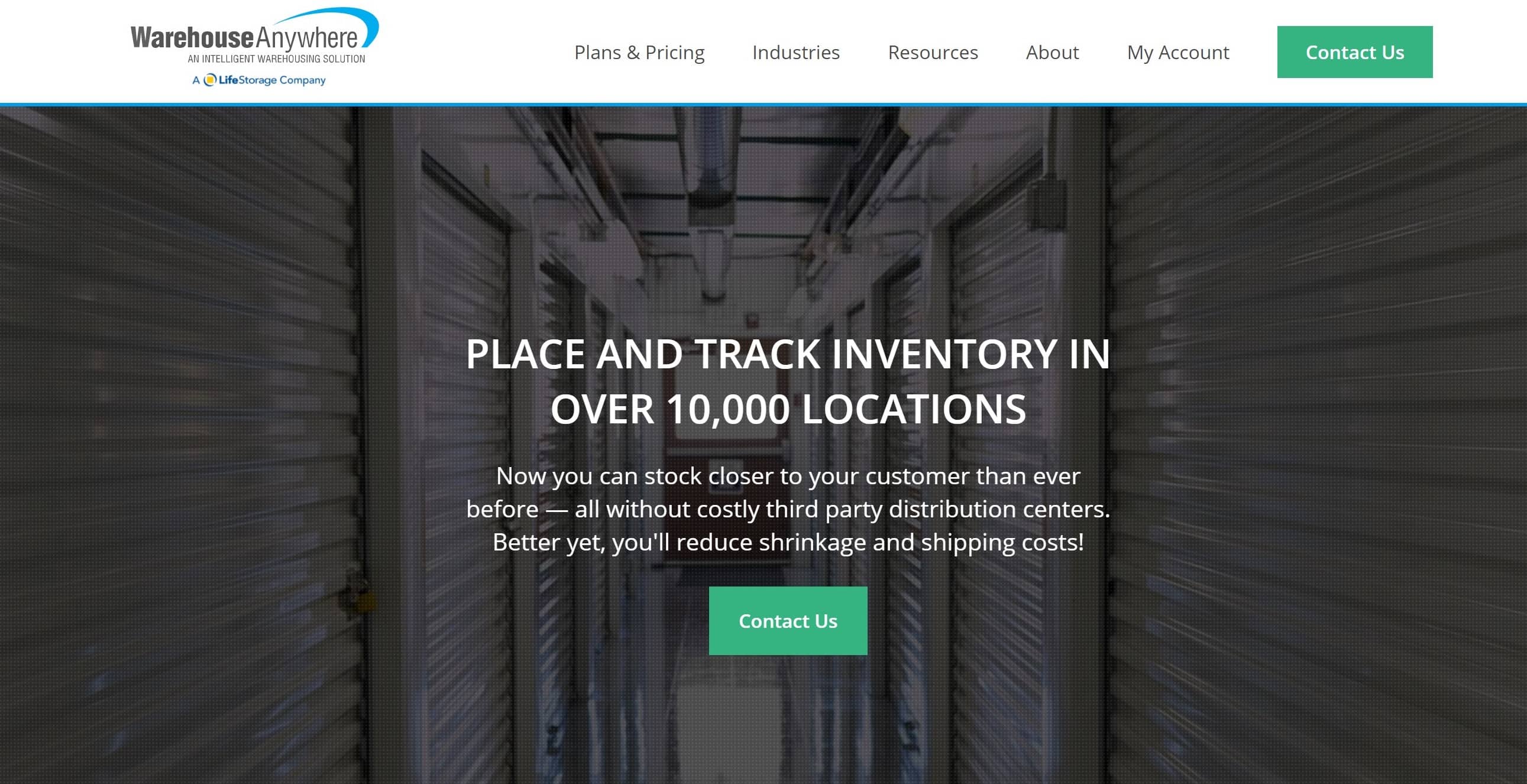

You guessed it, insiders made a move and bought stocks. On September 8th, one of PSA´s directors purchased more than 400.000 USD of shares at $214 per unit. This led me to go deeper into PSA and look at their earnings. Surprise! There were absolutely no mentions of the last mile logistics business segment, not in their fillings, not in the analysts Q&A, not in their annual report, nothing. They don´t even mention the B2B customers. Bummer... Ok, then which PSA competitor do take this opportunity seriously? The only direct competitor to PSA who has an actual plan to tackle that mega trend we just talked about is Life Storage (LSI). Life Storage has a product named "Warehouse Anywhere" dedicated to that Mega trend to attract business customers. It offers innovative inventory management tracking technology to support customers' supply chain and last mile delivery needs through data and tech. Here is what his CEO said in last earnings call back in August:

Warehouse Anywhere is an important tool for us to capture that business customer. No one else has it... The pipeline is very good. We had some hiccups trying to get the pilot programs conducted because of COVID related reasons. So we're kind of delayed a couple of months to what we expected this year... And again, I think storage is going to continue to play a role in last-mile delivery and logistics. So we're very excited that we own 100% of the business now and look forward to growing it.

Warehouse Anywhere has passed the validation period, has it already sells more than 6 Million USD from its platform fees, but it is still in the early days: LSI is a 575 Million USD business, so Warehouse Anywhere fees only account for about 1% of its revenues, but these fees are pure novel revenue stream, as this service was primarily designed to capture B2B customers who rent their storage space who account for 25% of their customer base.

Towards the "Platform" business model

I love the possibilities their "Warehouse Anywhere" platform model offers. Life Storage "only" has 900 storage facilities across the US, but their partner with another 10.000 third party storages that can be accessed, and invoiced, through Warehouse Anywhere. They also integrate with other third party services such as couriers and charge a commission on it. I can see in a near future Warehouse Anywhere transforming more and more toward a "platform as a service" where their customers could buy services such as insurances, couriers, labeling, printing and more.

Life Storage (LSI) Fundamentals: Value and dividends

According to SimplyWallSt´s discounted cash flows model, LSI is 10% undervalued 👍. I also like to look at the EV/Ebitda (Enterprise Value / Ebitda) ratio to evaluate the valuation of subscription/recurring businesses. Today LSI ratio is at 15.75, which is lower than his historic median of 19 👍, and lower than its competitors 👍. In terms of analyst outlook, the average consensus is a price target of 106.2 USD, which is about the same price as today 👎.

LSI also pays a generous 3.9% dividend 👍, which is very positive in the current low bond yields market, where investors are hunting for more yield.

For all of the above, and the fact LSI average revenue growth in the past 3 years is 7.5%, I do think LSI is a value stock with a growth asset under the sleeve (Warehouse Anywhere).

Following is a list of other things I look at before investing in a stock, partly inspired by the "Antifragile" and "Quality score" frameworks from Motley Fool´s analyst Brian Stuffel and Brian Feroldi:

- Financial Strenght 👎 for now: LSI's debt to equity ratio (95.2%) is considered high and has increased from 75.9% to 95.2% over the past 5 years. Debt is not well covered by operating cash flow (13.9%). Interest payments on its debt are not well covered by EBIT (2.9x coverage). Profit per employee is also lower than its peers (PSA, EXR, CUBE) at $200.000 vs an average of $220.000. My guess is this metric will improve in the short term as LSI has developed a completely digital, contact free, self-serve model to allow customers to “skip the counter” and support social distancing, which represents about 30% of all its bookings today. There is also a very positive trend, indirectly related to their Rent Now tech, which is their marketing acquisition cost (total moves-in / total marketing spend) lowered from $18 in 2019 to $13 in 2020.

- Culture and management 👎: CEO approval rate is low at 38% (Source: Glassdoor), individual insiders ownership is low at less than 1%, but the average leadership position tenure is high at 11 years.

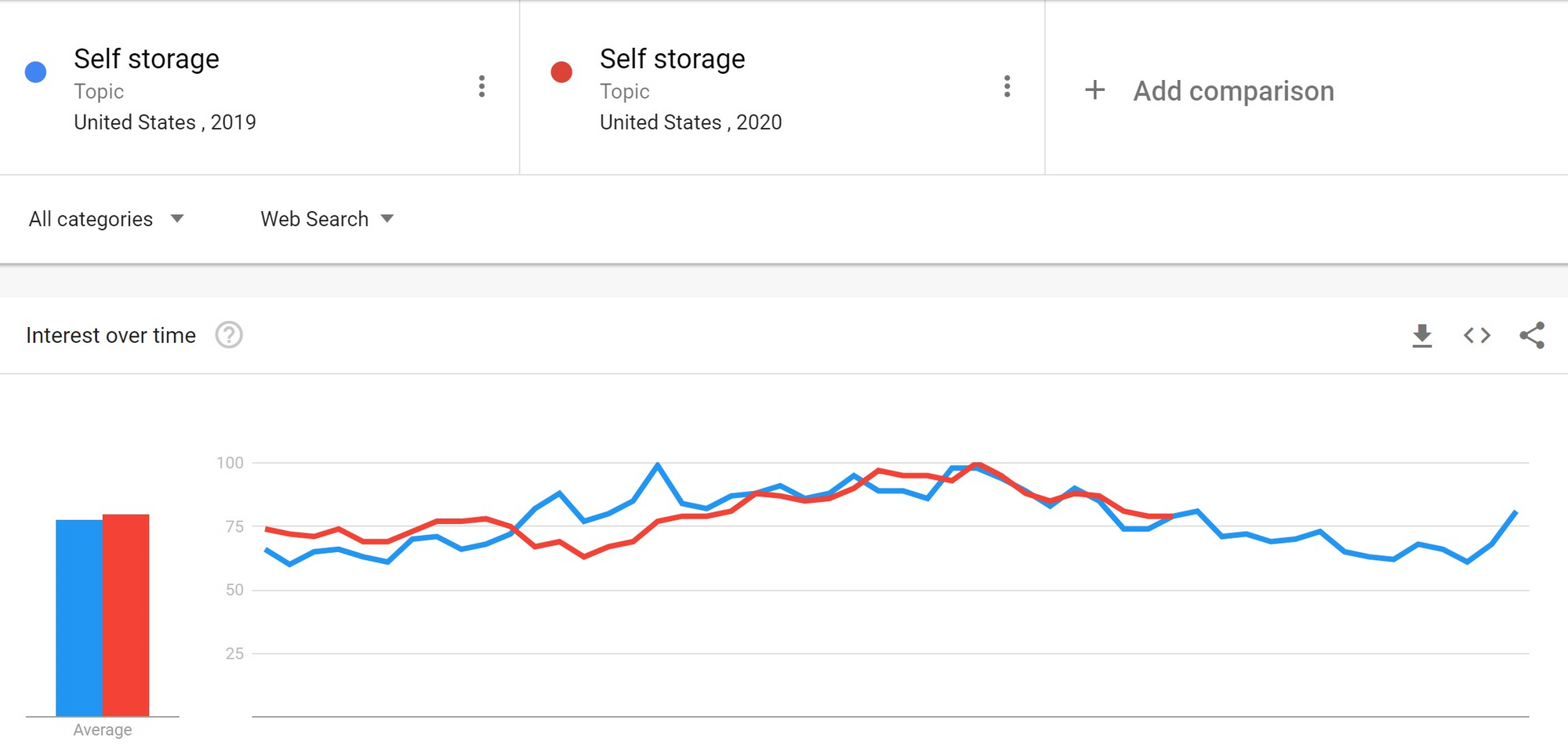

- Momentum 🤏: Revenue decreased last quarter -2%, which is not that bad giving the last quarter COVID impact. Plus, the demand for self storage has started increasing again since June. There is currently a hiring surge (Source: Glassdoor), and Hedge Funds increased holdings by 228.9K shares last quarter (Source: TipRanks). Of course, revenue growth is not mindblowing (+7.5% average in the past 3 years), which is precisely why this is the kind of stock called "value stock". Last but not least, the fact that a direct competitor insider bought shares of PSA is a good signal.

- ESG Risk rating (source: Sustainalytics) is Low 👍

- Moat (how difficult it is to copycat) 👍: Network effect is high as the more storage it has the more value it can provide to their B2B customers´ logistics and the more variables it will have for its inventory optimization services. Switching costs for its customers is huge as it means moving out and moving in again at another storage. They are not in an industry where we can say they have a low-cost production, but their Rent Now platform is sure the way to go for lowering their operation costs compared to their competitors, and they seem to be the first one to have invested in that direction (even though they now all have it). As far as intangible assets are concerned, I am not aware of any patent, nor incredible Brand Value, less so government protection. What I do see as a valuable intangible asset is its Warehouse Anywhere technology and its data science team experience and data collecting.

What are the risks and when would I sell?

Life Storage may be the only self storage company to offer distribution center oriented solutions, but it not the only one outside of the self storage industry. There are monster industrial REITs with a lot more real estate and firepower such as Prologis (PLD), who even provides distribution centers to Amazon. Plus, experts project that some Malls will be reimagined as distribution centers, which means that Malls REITs would increase competition for Warehouse Anywhere, but it is still unsure what will happen for Malls.

Prologis is way better positioned for the big retailers, but I think Warehouse Anywhere is more accessible to small and medium businesses, but it is still to see if these smaller businesses can afford to have more than 1 inventory location.

Growth will be the main metric of success for their Warehouse Anywhere business, and I would sell if I do not see triple digits growth.

I am buying a full position on LSI of about 2% of my portfolio

If you want to see my live portfolio, see my stats, or even copy my trades, you will need an account with eToro, which is the broker I use. In case you do open an account with eToro, use this referral link, let me know and you win 100 USD cash. If you have an account, you can look for me by my username "Nrikike".

If you like my content you can subscribe for free and follow me on Twitter.

The author of this post owns shares of Life Storage. The Rookie Investor recommends Life Storage. The Rookie Investor has a disclosure policy.