Insider👁🗨 alert: opportunities in the digital transformation of the Banking industry.

Insiders just did the work for me yet again, showing me where to prioritize my analysis. This time, the name that popped up from my watchlist is Jack Henry Associates (JKHY), as one of its Directors bought 1.4 million USD of stocks on December 22nd at an average $156 per share. This company was on my watchlist already as it is well positioned for helping US Financial Institutions with their own "digital transformation" efforts, which the pandemic has leap-frogged. So let´s go deep into Jack Henry to see if it´s worth investing in.

What is JKHY business about?

In their own terms, the 40 years old company is a "leading provider of technology solutions primarily for the financial services industry." They serve about 9,000 US clients through three divisions: Jack Henry Banking® supports banks ranging from community banks to multi-billion-dollar institutions; Symitar® provides solutions to credit unions of all sizes; and ProfitStars® offers specialized solutions to financial institutions of every asset size. They claim to be "well-positioned as a driving market force in future-ready digital solutions and payment processing services".

So basically, Jack Henry is a major actor in the digitization of banking services in the US, particularly for regional & community banks and credit unions. With hundreds of products and services, they can help to build a bank from the ground up or enhance the operations of an established player with billions in assets, from Mobile Banking App to fraud detection. Kind of a Banking-as-a-Service player with an unmatched level of customization according to their client needs.

Relevant Macro Trends impacting the stock

Tailwinds

Small banks in the US are big business. Community banks account for 97% of all bank charters and account for around $2.9 trillion in assets. Trillions of dollars more are accounted for by regional banks. Then there are the credit unions that are adding customers in record numbers, up 21 percent over the past five years. In loan origination, credit cards, and mortgages, credit unions are gaining market share and around 1 in 4 Americans have used them. Giving the impressive number of clients Jack Henry has, most of these institutions are their clients.

But the biggest tailwind is probably the pandemic itself, and its acceleration effects on the digitization/automation, branch shutdowns, and customer-facing digital banking penetration. According to the Bank Director Technology Survey from August, most banks had moved 2 items to the top of their priority list: improved customer experience and improved set of digital offerings. Jack Henry bought a Fintech named "Banno" about 5 years ago, it consists of a white-label mobile banking app. This positions them as a key partner for smaller banks that need to compete with the greatest digital experiences offered by Neobanks. Besides an advanced UX , one key component of this app is the "Banno conversations" feature, which allows the small financial institution to maintain their edge in 1-1 personalized customer service in a remote way. The app users can start an encrypted text message with the customer support rep. that's encrypted, so they can actually share bank data, which is not a given in most of the chat providers giving the heavy security protocols the banking industry has.

The pandemic also impacted the way Americans pay, favoring debit over credit cards. Here there is one very interesting opportunity that arises from the current regulation referred to as the "Durbin Amendment". This piece of regulation caps the interchange fees debit card issuer can charge merchants, but only for issuers with a market capitalization of over $10 billion. The vast majority of Jack Henry´s customers are below the $10 billion market cap, which means they have greater freedom to offer juicier rewards for the end user of their debit card than big banks. This offers a clear opportunity to grow its debit card business. Jack Henry has been working for the past 2 years on a solution to integrate both credit card and debit card processing for their customers, and they started to migrate the first customers to such a platform. All of this bodes very well for the company payments solution growth for the foreseeable future.

Headwinds / Risks

The ~10.5K small US banks and credit unions have been steadily declining at a 3 to 4% annual rate since the late 90s, primarily from mergers & acquisitions in search of economies of scale. The potential accelerating of such consolidation could make some of Jack Henry’s customers disappear in the medium term.

Plus, a new generation of Neobanks (e.g., Cash App, Chime) reached critical mass this year and turned up the heat for the race to become the preferred bank for Americans. 8 of the top Neobanks in the US have increased} their user bases by ~35mm up +32% YTD through Q3 2020. This is a clear risk for Jack Henry to see their clients lose ground long term, but it may actually boost their prospect short to medium term. Their management made a quite interesting parallel of the opportunities it gives them: "I'll go back to the complete online digital lending platform that we rolled out a couple or 3 years ago. We did that because we saw what was happening with OnDeck and Kabbage and the potential for those solutions to disintermediate the commercial borrower from our customers. We were very successful in helping those customers who needed to fend off those competitors, and we'll do similar things here as we see those opportunities. We are up to installing 40 Banno solutions a month, but out of our 1,700 plus core customers, less than 400 of them are on Banno platform today. So there's a huge upside there."

Interesting patterns in Insiders Buyings

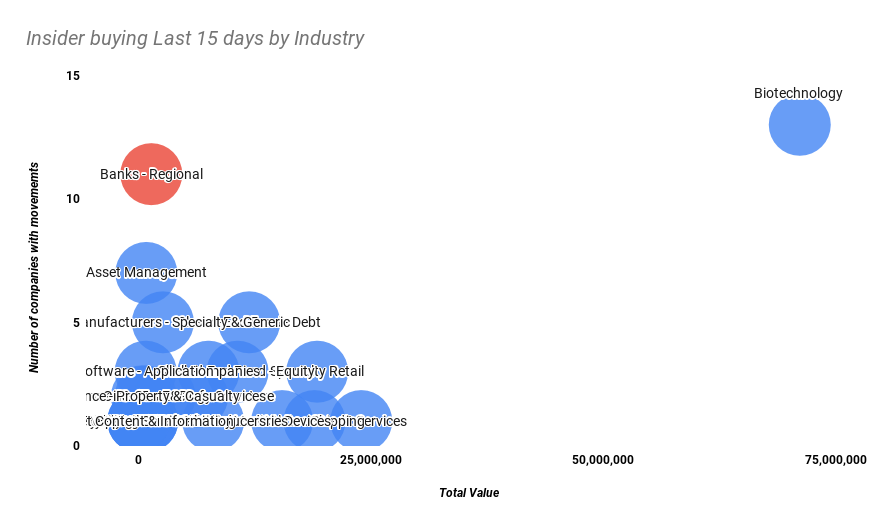

Tracking insiders´ moves are my favorite strategy to invest, and I recently started to track their buying moves aggregated by sector. Guess what? in the past 2 weeks only, no less than 13 insiders have bought for more than 10K USD of shares of 11 different regional banks... Now do I have your attention?

JKHY Fundamentals

Moat & Potential: 9/12

Contracts in this business last 5 years+, the cost of switching systems is huge, and their cost measured in debt to equity and SG&A % of revenue is lower than its peers. Jack Henry manages to maintain sticky relationships with just 1-2% of banks changing core providers per year, Jack Henry’s consistently robust top-line performance has been driven by share gains in core account processing as the vast majority of these core customers purchase 20-30 additional products, driving growth across the rest of the business, and making JKHY the king of the hill in terms of cross and upselling.

Here is what their management has to say about it: "we have a very long history of continuing to cross-sell products. We have such a broad suite of products that over the life of the relationship, we just continue to sell more and more and more to those customers."

They also manage decent optionality and potential. Their vision to "use technology to enhance the community banking model across every customer touchpoint" allows for multiple ways to grow business. Even though it is limited to small banks, their organic growth runway is still large within it. The company has demonstrated that it can tinker with new products and create value such as with the purchase of Banno.

Financial fortitude and risk management: 2/2

They carry almost no debt and operate with a solid cash position. Their revenue is more than 85% recurring in nature. Their dividend yield is low at about 1%, but they say they will continue to increase it, just like they have done it for the last 29 years, and they will continue to buy back stock.

Their customers are numerous thus not concentrated, they have a low ESG risk according to sustainalytics and they are also free from geopolitical risk.

Skin in the game and culture: 0/3

Even though their glassdoor rating is high at 3.6, with a 86% CEO approval, there is very little skin in the game as Insiders own less than 1% of the company and have less than 5 years in the role.

Momentum & Valuation: 0/2

Revenue growth has been stable between 5 and 9% since 2014. The company is currently fairly valued according to GuruFocus model, but Hedge Funds have decreased their positions in the last Quarter. Analysts are less than bullish with it, with a mean price target just about 10% higher than today´s price and many "hold" ratings.

Final thoughts

Giving all the insider signals and Jack Henry strong moat, I think it´s a buy even if analysts are rather cautious with this stock. I already have a small position in it but will be adding to it in the next few weeks to build a full position of about 2% of my current portfolio.

If you want to see my live portfolio, see my stats, or even copy my trades, you will need an account with eToro, which is the broker I use. In case you do open an account with eToro, use this referral link, let me know and you win 100 USD cash. If you have an account, you can look for me by my username "Nrikike".

If you like my content you can subscribe for free and follow me on Twitter.

The author of this post owns shares of Jack Henry. The Rookie Investor recommends Jack Henry. The Rookie Investor has a disclosure policy.